Flood Zones in New Braunfels: A Homebuyer's Guide

Before you buy near the Comal or Guadalupe River, here's what you need to know about FEMA flood zones, insurance costs, and how to protect your investment.

New Braunfels is defined by its rivers — the Comal and the Guadalupe are two of the biggest reasons people move here. But before you fall in love with a property near the water, there's a critical layer of due diligence that too many buyers skip: understanding FEMA flood zones and what they mean for your insurance costs, your mortgage, and your long-term investment. This guide breaks it all down so you can buy near the water with your eyes wide open.

FLOOD ZONE BASICS

How FEMA Flood Zones Work — and Why They Matter Here

The Federal Emergency Management Agency (FEMA) maps flood risk across the country through its National Flood Insurance Program (NFIP). These maps, called Flood Insurance Rate Maps (FIRMs), assign properties to flood zones based on their statistical likelihood of flooding in any given year. In a city built around two rivers, those designations carry significant financial and practical weight.

The Zone Designations You'll Encounter

FEMA flood zones are labeled with letters, and each letter tells a different story. Zone X (or Zone C on older maps) is the lowest-risk designation — properties here are outside the 500-year floodplain, and federal flood insurance is not required. Zone AE is the most common high-risk designation in New Braunfels: it sits within the 100-year floodplain, meaning there's a 1% or greater chance of flooding in any given year. Zone VE applies to coastal areas with wave action, which is not relevant in New Braunfels. Zone A is similar to AE but lacks detailed engineering data. Zone X (shaded) denotes moderate risk — the 500-year floodplain — where insurance is optional but sometimes wise.

What 'Special Flood Hazard Area' Actually Means

Any property in Zone AE or Zone A falls within what FEMA calls a Special Flood Hazard Area (SFHA). If your home is in an SFHA and you have a federally backed mortgage — which includes most conventional loans, FHA loans, and VA loans — your lender is legally required to mandate flood insurance. This is not optional and cannot be waived. The designation follows the land, not the structure, so even if the home has never flooded, you'll still pay if the map says you're in the zone.

LOCAL GEOGRAPHY

Which New Braunfels Areas Are Most Affected

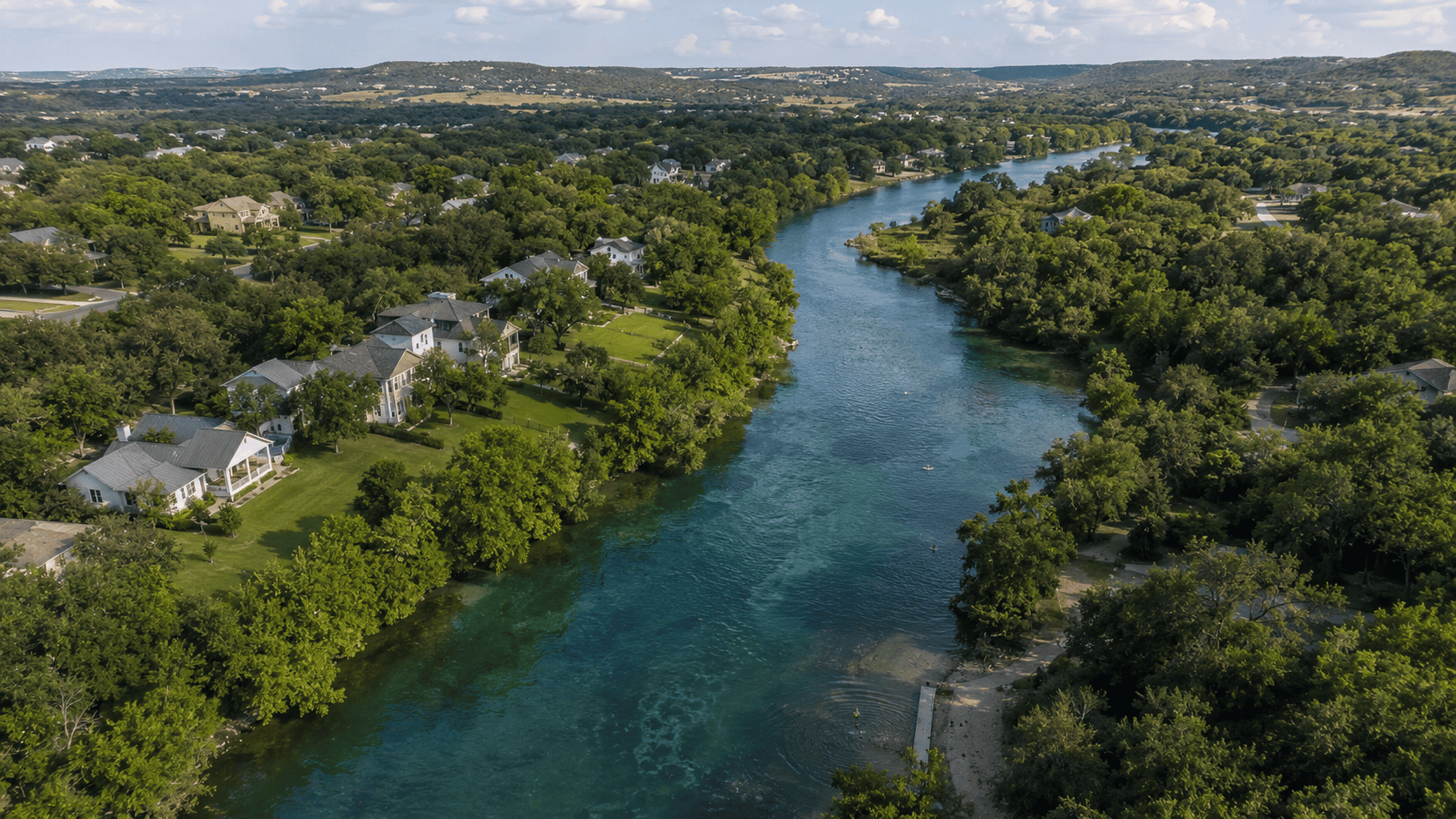

Because New Braunfels sits at the confluence of the Comal and Guadalupe Rivers, flood zone exposure is a real and ongoing reality for a meaningful portion of the housing market. Understanding which general areas carry elevated risk helps buyers target their search more deliberately.

The Comal River Corridor

Properties along the Comal River — particularly those closest to Landa Park and the stretches running through downtown — have a notable presence in Zone AE designations. The Comal is one of the shortest rivers in the world, but its flow is spring-fed and can surge quickly during heavy rainfall events. Neighborhoods and subdivisions with rear lots or easements bordering the Comal should be scrutinized carefully, even if the home itself appears to be set back from the water.

The Guadalupe River and Upstream Tributaries

The Guadalupe River, which runs along the southern and eastern edges of New Braunfels before passing through Canyon Lake Dam downstream, creates a wider flood corridor. Areas near River Road, Gruene Road, and stretches of FM 306 closer to the river carry significant AE zone designations. Properties marketed as 'riverfront' or 'river access' near the Guadalupe should be assumed to carry flood zone exposure until verified otherwise. Upstream events and dam releases from Canyon Lake can also affect river levels rapidly and with little warning. Several smaller creeks and drainageways throughout Comal County — including Dry Comal Creek — also carry AE or A designations that can affect inland properties buyers wouldn't expect.

Areas Generally Outside the Flood Zone

Much of the master-planned and newer residential growth in New Braunfels sits on higher ground and is designated Zone X. Neighborhoods like River Chase (where Todd Spencer lives), Vintage Oaks, Veramendi, and newer developments in the FM 3009 and FM 1101 corridors are largely in lower-risk zones. This doesn't mean those areas are immune to localized drainage issues, but they typically don't trigger mandatory federal flood insurance requirements.

DUE DILIGENCE

How to Look Up a Property's Flood Zone Before You Make an Offer

Buyers don't need to wait for a lender or an agent to tell them a property's flood zone status. There are free, publicly accessible tools that put this information at your fingertips — and using them early in your search can save significant time and money.

FEMA's Flood Map Service Center

The primary resource is FEMA's Flood Map Service Center at msc.fema.gov. You can search any address and pull up the current FIRM panel for that location. The map will show the flood zone designation and the effective date of the map. One important caveat: FEMA maps are not always current. They can lag behind real-world conditions by years, and some areas in Comal County have pending map revisions. Always look at the map effective date and ask your agent whether any Letters of Map Amendment (LOMAs) or Letters of Map Revision (LOMRs) have been filed for the property.

Comal County and City Resources

The City of New Braunfels participates in FEMA's Community Rating System (CRS), which can provide discounts on flood insurance premiums to residents. The city's planning and development department can provide flood zone information and answer questions about local drainage studies. Comal County Appraisal District records and the county's GIS portal also overlay flood zone data on parcel maps, which can help you visualize how close a specific property sits to zone boundaries. Your title company will note flood zone status in the title commitment as well.

Working with a Flood Zone Specialist or Surveyor

If a property is near a zone boundary — or if the seller claims it was recently removed from a flood zone — it is worth hiring a licensed surveyor to produce or verify an Elevation Certificate. This document precisely measures the lowest floor of the structure relative to the Base Flood Elevation (BFE) established by FEMA. An Elevation Certificate is required to accurately rate flood insurance, and it can sometimes reveal that a home's actual elevation qualifies for significantly lower premiums than the zone designation alone would suggest.

INSURANCE & COSTS

What Flood Insurance Actually Costs in New Braunfels

Flood insurance is one of the most misunderstood costs in real estate transactions. Many buyers assume their homeowner's policy covers flood damage — it does not. Flood insurance is a separate policy, and in high-risk zones, it can meaningfully affect your monthly housing costs.

NFIP vs. Private Flood Insurance

The National Flood Insurance Program (NFIP), administered by FEMA, was historically the primary source of flood coverage for most homeowners. NFIP policies max out at $250,000 for the structure and $100,000 for contents. In 2021, FEMA introduced Risk Rating 2.0, a new pricing methodology that bases premiums on the individual property's specific flood risk — including distance to water, elevation, and flood frequency — rather than just the zone designation. This has caused premiums to change significantly for many properties, with some seeing increases and others seeing decreases. Private flood insurance has grown substantially as an alternative, often offering broader coverage, higher limits, and sometimes lower premiums than NFIP for the same property.

What to Budget

Under FEMA's Risk Rating 2.0 methodology, NFIP premiums in New Braunfels for high-risk Zone AE properties commonly range from $1,200 to over $4,000 per year depending on the property's specific characteristics. Homes with lower elevations relative to the BFE, or those with finished basements or lower-floor living spaces, tend to sit at the higher end. Properties in Zone X pay substantially less if they choose to carry coverage — often in the $400–$800 annual range for a standard NFIP policy. Private market alternatives can sometimes undercut NFIP rates by 20–40% for well-elevated homes. These are budgetary estimates — actual quotes require a licensed insurance agent and, for accurate pricing, an Elevation Certificate.

MORTGAGE IMPACT

How Flood Zones Affect Your Mortgage and Closing

Flood zone status is not just an insurance issue — it has direct implications for your loan terms, your closing timeline, and your ability to finance certain properties. Lenders are required by federal law to identify flood zone status before closing any federally backed mortgage.

The Mandatory Purchase Requirement

Under the Flood Disaster Protection Act of 1973 and subsequent legislation, lenders originating federally backed mortgages must require borrowers to purchase and maintain flood insurance for properties in Special Flood Hazard Areas. This requirement stays with the loan — if you refinance, the new lender will also confirm flood zone status and insurance. If a property is in an SFHA and you choose not to maintain flood insurance, the lender can force-place a policy on your behalf, which is typically far more expensive and less comprehensive than a policy you'd obtain yourself.

Appraisals, Underwriting, and Timing

Flood zone determination happens as a routine part of mortgage underwriting, typically through a third-party flood zone determination service hired by the lender. The cost (usually $10–$25) is passed to the borrower in closing costs. If the determination changes between contract and close — as can happen near zone boundaries — it can delay closing while insurance is obtained and underwriting is updated. Building in adequate time for this process is especially important in New Braunfels, where flood zone boundaries can run through or adjacent to established neighborhoods. Todd Spencer routinely flags potential flood zone exposure early in the transaction so buyers have time to shop insurance and avoid last-minute surprises at the closing table.

SMART BUYING

Questions to Ask Before Buying Near Water in New Braunfels

Waterfront and water-adjacent properties remain some of the most desirable listings in New Braunfels — and for good reason. River access, views, and the lifestyle they offer are genuinely special. But buying smart near water requires asking the right questions before you're emotionally committed to a property.

What to Ask the Seller and Their Agent

Start with the basics: Has the property ever flooded? When? How much water entered the structure? Ask for documentation — insurance claims, permits for repairs, or contractor records. Texas sellers are required to disclose known flooding history under the Texas Seller's Disclosure Notice, but disclosure is only as good as the seller's knowledge and honesty. Ask whether the property has an Elevation Certificate on file, and whether the seller currently carries flood insurance and at what cost. If the seller's premium seems unusually low, find out why — it could indicate a LOMA on file that removed the property from the mandatory purchase zone, or it could indicate undisclosed risk.

What to Verify Independently

Pull the FEMA flood map yourself. Order an Elevation Certificate if one doesn't already exist — a licensed surveyor can produce one for roughly $500–$900, and it's money well spent before committing to a six-figure purchase. Ask your insurance agent for an actual flood insurance quote before your option period expires, not after. Check the property's claims history through a CLUE (Comprehensive Loss Underwriting Exchange) report, which your insurance agent can request. And research whether the area is subject to Canyon Lake Dam release protocols, which can rapidly elevate Guadalupe River levels downstream — sometimes with little public notice to homeowners.

Understanding Elevation Certificates

An Elevation Certificate is a standardized FEMA form completed by a licensed land surveyor that documents a building's elevation relative to the Base Flood Elevation on the current FIRM. It is the single most important document in determining your actual flood insurance premium. If a home sits well above the BFE — even if it's technically in Zone AE — the Elevation Certificate can demonstrate that reduced risk to your insurance carrier and result in substantially lower premiums. Some properties have elevation certificates on file from prior transactions; others will require a new survey. Always ask for it, and if it's more than five years old, verify that no FIRM revisions have occurred since it was issued.

Common questions

Frequently asked questions.

Is all riverfront property in New Braunfels in a flood zone?

Not necessarily, but the vast majority of properties directly adjacent to the Comal and Guadalupe Rivers carry some level of FEMA flood zone designation, and most fall within Zone AE — the highest-risk category for non-coastal areas. The flood zone boundary doesn't always align perfectly with the riverbank; some properties set well back from the water are still within the SFHA, while occasional parcels right at the water's edge have been removed through elevation studies or Letters of Map Amendment. The only definitive way to know a specific property's status is to search the address on FEMA's Flood Map Service Center or ask your agent to pull the flood determination. Never assume based on visual distance from the water alone.

Can I buy a home in a flood zone without purchasing flood insurance?

If you're financing the purchase with a federally backed mortgage — which includes conventional loans, FHA, VA, and USDA loans — the answer is no. Federal law requires lenders to mandate flood insurance as a condition of the loan for any property in a Special Flood Hazard Area. If you're purchasing with cash, flood insurance is technically optional, but declining it would be a significant financial risk in an area with demonstrated flooding potential. Even a modest flood event can cause tens or hundreds of thousands of dollars in damage, and standard homeowner's policies explicitly exclude flood damage. Cash buyers should think of flood insurance not as a lender requirement but as fundamental risk management for the asset.

How much does flood insurance cost for a home near the Guadalupe or Comal River?

Under FEMA's Risk Rating 2.0 pricing model, premiums are now calculated based on individual property characteristics rather than just zone designations, so there's no single answer that applies to all riverfront homes. That said, Zone AE properties in New Braunfels commonly see NFIP premiums ranging from around $1,200 to $4,000+ annually depending on the home's elevation relative to the Base Flood Elevation, the type of foundation, and the presence of any enclosed lower-level areas. A home that sits several feet above the BFE will cost significantly less to insure than one at or below it. Private flood insurance alternatives can sometimes offer competitive pricing, especially for higher-value homes that need coverage above NFIP's $250,000 structural limit. The only way to get an accurate number is to request a quote from a licensed insurance agent who has access to your Elevation Certificate.

What is an Elevation Certificate and do I really need one?

An Elevation Certificate (EC) is an official FEMA form completed by a licensed land surveyor that documents exactly how high your home sits relative to the Base Flood Elevation established on the current FIRM. It is used by insurance carriers to calculate your actual flood insurance premium, and without one, insurers must assume worst-case elevation data — which typically results in a significantly higher quote. If a property already has a recent EC on file, it can be transferred to a new owner at no cost. If one doesn't exist or is outdated, a new survey typically costs $500–$900 in the New Braunfels area. For any purchase in or near a flood zone, Todd Spencer recommends obtaining or verifying an Elevation Certificate before the option period expires — it's one of the most cost-effective pieces of due diligence a buyer can do.

Can a property be removed from a FEMA flood zone?

Yes — this process is called a Letter of Map Amendment (LOMA) for individual properties or a Letter of Map Revision (LOMR) for larger areas, and it's more common than many buyers realize. If a property's actual ground elevation is higher than what FEMA's flood maps show, the owner or a surveyor can submit an elevation study to FEMA requesting that the property be formally removed from the SFHA. If granted, the mandatory flood insurance purchase requirement is lifted for that property, though voluntary coverage is still available. A property with a LOMA on file is worth understanding carefully — ask the seller for the documentation, verify it's still valid under the current FIRM, and decide independently whether you still want some level of coverage even without the federal mandate.

How does New Braunfels handle flood risk as a city — is anything being done?

The City of New Braunfels participates in FEMA's Community Rating System (CRS), a voluntary program that rewards communities for implementing flood risk reduction measures beyond minimum federal requirements. CRS participation earns residents discounts on NFIP flood insurance premiums — typically ranging from 5% to 45% depending on the community's rating class. The city has also invested in drainage infrastructure improvements and updated floodplain management ordinances in recent years. Comal County has conducted localized drainage studies along key waterways, and some areas have undergone map revisions as a result of new engineering data. Buyers can contact the City of New Braunfels Floodplain Administrator directly for information about ongoing studies or planned infrastructure projects that might affect specific areas.

Ask Todd

Have a specific question?

The honest answer is usually faster than a long article. Send a note and I will reply within a business day.